Yum China: A Hidden Gem in Quality Investing

The Potential of Yum China – A Growth Powerhouse with Strong Fundamentals

Fast Food chains are great businesses. They offer high ROIC, high brand awareness all around the world and have a track record of creating shareholder value. The problem is, that you have these businesses on your watchlist and follow them closely. But they never get cheap enough to make a well thought decision. Once you forget about them, they will make a new all time high in silence. KFC has one of the best brands in the world and we can currently invest into a portfolio of world class brands, growing quickly at an attractive price. In the following piece, we will take a look at Yum China. The business has been doing terrific over the last months, while the stock sold of hard. This is one of the lowest risk investments in China, that can provide us access to the Chinese middle class.

1.0 Overview YUMC 0.00%↑

Yum China is the Chinese division of Yum Bands that was spun of in 2016. Their main brands included KFC, Pizza Hut, Taco Bell and LavAzza. The current CEO is Joey Wat, and the company has a total store networks of 14.100 stores at the moment. The current market cap is around 14.3 Billion $, the stock trades at 35$ a share. YUMC 0.00%↑ has set ambitious goals in terms of growth and shareholder distributions. The main question has been, wether the company can substation growth with slowing economic growth in China. The answer is clearly yes. Over the past 4 yers the company opened around 5000 stores, increased efficiency and reduced CAPEX per store.

2.0 China’s Middle Class and Scale

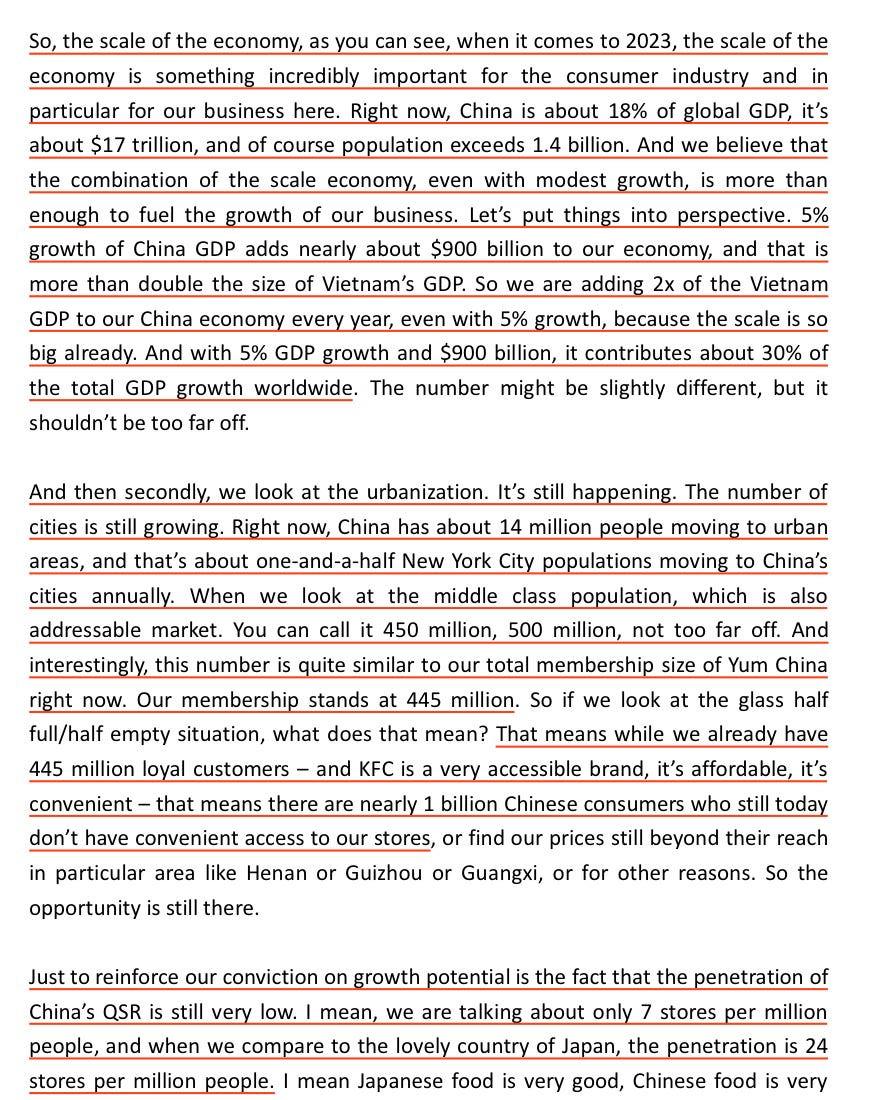

While there is a lot of trash talk about the Chinese economy, we have to emphasize that the economy of China is already huge. With a GDP of 18 Trillion $, we shouldn’t underestimate how much scale the economy already has. In the recent Q3 earnings call, Joey said the following about China’s economic growth and scale.

To summarize the main points, at a 5% growth rate, the Chinese GDP would grow 2x the GDP of Vietnam in the timeframe of a year ! Every year around 14 million people move to urban areas and there are on average 7 stores per 1 million people in China, while this number stands at 24 in Japan.

Regarding the Middle Class I wrote about it in more detail in this piece 👇

China’s address on global demand and the Middle Class

Davos is a place we’re billionaires, politicians and or psychopaths meet once a year. Often times I ignore to listen to the wide variety of speeches held there, since it’s often just a waste of time. But this time, there have been several speeches that surprised me in particular. One of them being the great speech by Javier Milei about socialism, the de…

China's PM Li Qiang mentioned the rise of China’s Middle Class in his recent speech at Davos too.

"In China, there are now over 400 million people in the middle-income bracket, and the number is expected to reach 800 million in the next decade or so. For a growing range of products and services, the focus of consumer demand is shifting from quantity to quality, which will generate strong driving force for upgrading consumption. There are also some 300 million rural migrants who are acquiring permanent urban residency at a faster pace. These will create massive demand in areas such as housing, education, medical services and elderly care."

— Li Qiang, Davos January 16th 2024

3.0 Growth & Efficiency

So the demand for Restaurants will continue to grow rapidly. As a result, YUMC announced a target of 20.000 stores by 2026 and cumulative shareholder distributions of 3 Billion $ till 2026.

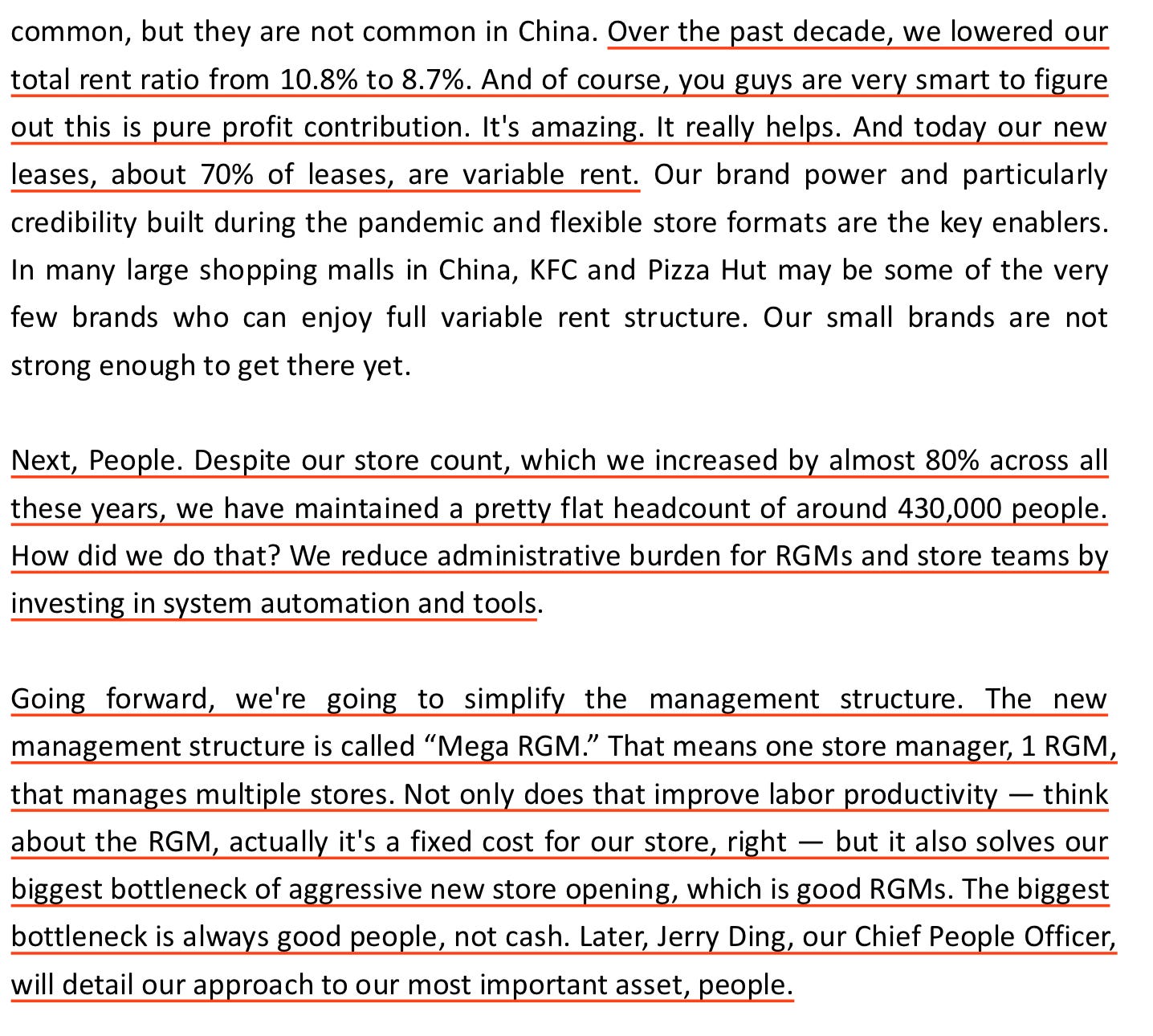

This would mean an acceleration of growth in the coming years. The reason for this is increased scale and efficiency. The upfront cash investment per KFC store has dropped by 50% from 3 million RMB to 1.5 million over the period of 7 years. For Pizza Hut these numbers are even more insane with a reduction of 60% from 3 million RMB to 1.2 million. The payback time is currently 2 years for KFC stores and 3 years for Pizza Hut stores. These are great numbers and demonstrate the capital allocation discipline by the management team. To increase efficiency further, digital orders are now accounting for 90% of sales. While store count has gone up by 80% since 2016, the number of employees has remained flat.👇

Variable rents are also beneficial for the company as rents are a large part of costs associated with running a restaurant chain. To achieve the goal of 20.000 stores, the supply chain needs to be optimized. The company is building a logistical network to cover 5000 cities. By cooperating with suppliers, costs will be cut and delivery times reduced. The automation of the Xiˋan logistics center for example, is expected to increase storage capacity by 50%, reduce delivery time by 51% and increase operational efficiency by 45%. The combined factors mentioned, make the management team confident, that their ambitious targets will be achieved by 2026. As Joey mentioned in the Q3 call, the number of Restaurant Managers (RGMs) will not increase as much as the store count, since the company is already reducing the time RGMs lose in the process of finding new personal. This frees up time, which in turn enables them to manage not only one, but two or possibly up to three locations.

4.0 Financials

Yum China has suffered during the pandemic, which affected basically their entire business model. But the company has been able to recover from this setback and is on track to expand the company’s brands across all of China.

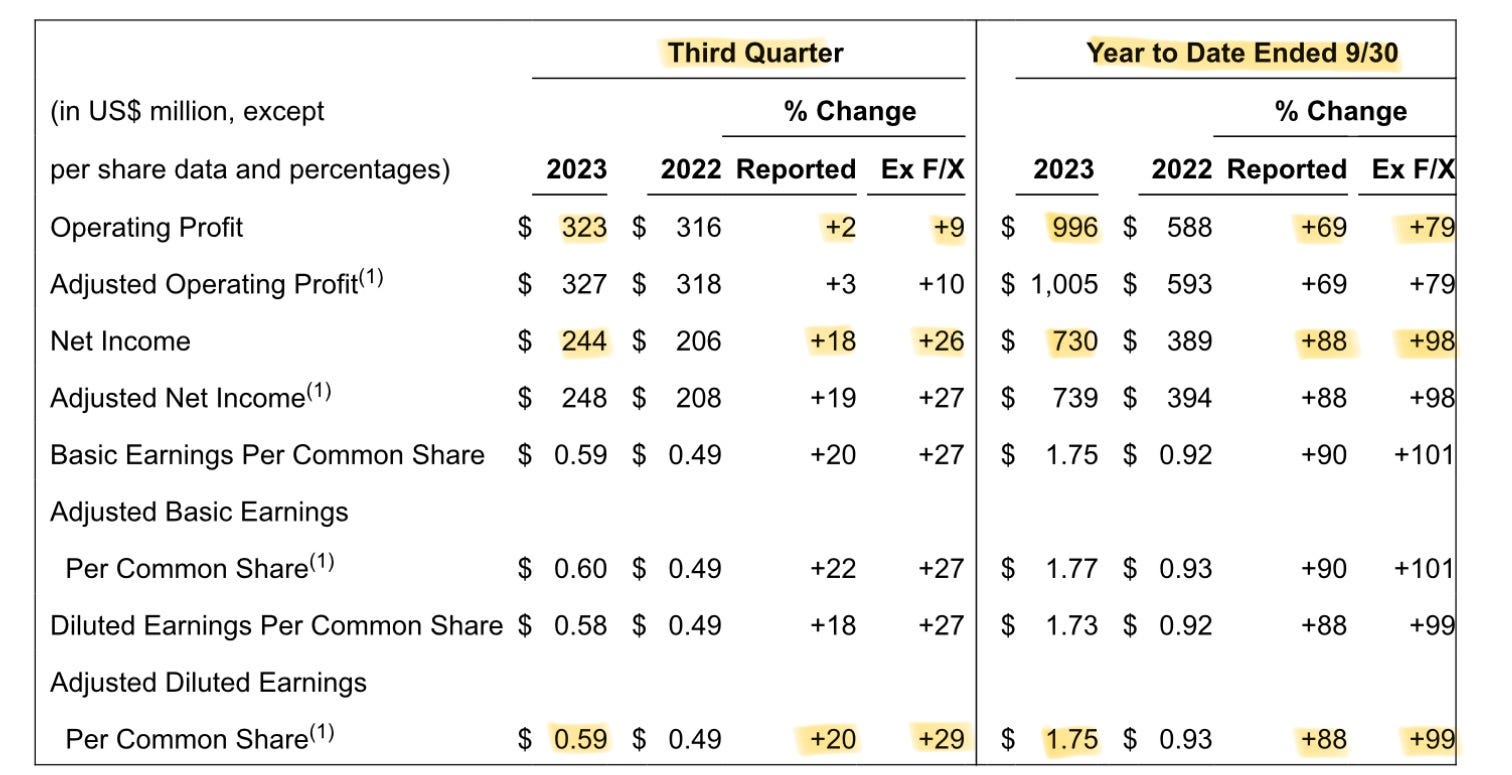

In the 3rd quarter revenues went up by 15% in constant currency and 9% in USD. Net Income went up by 18% reported and 26% excluding foreign exchange rates. EPS appreciated by 20 and 29% respectively to 0.59$. Year to date earnings appreciated by 80 to 100% in different metrics, as the company recovered from COVID lockdowns.

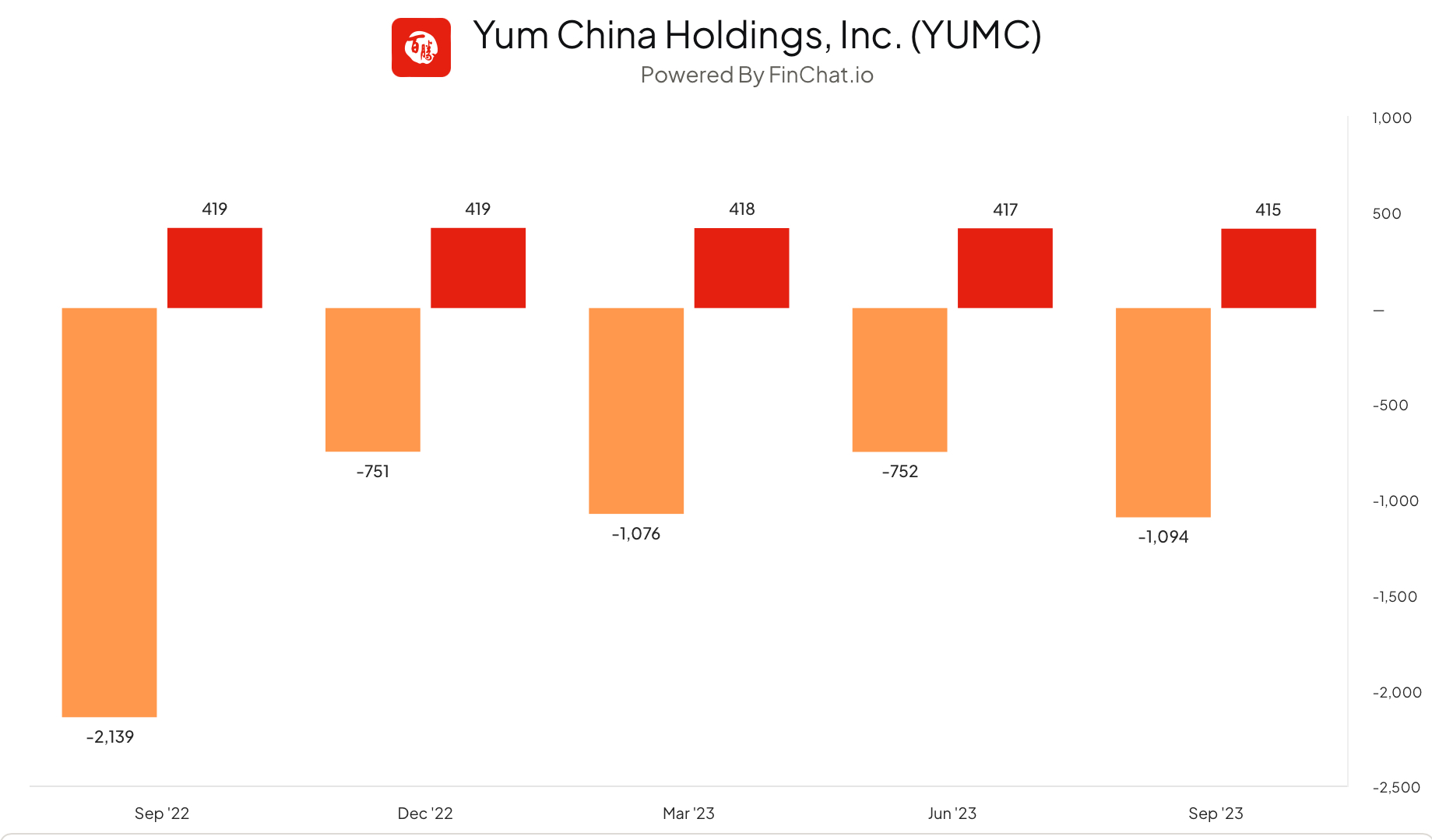

Year to date (3 quarters) Yum China generated FCF of 835 million USD. The Balance sheet of Yum China is very strong, as the company has a net cash position of around 1.1 Billion USD. Below we can see the Net Debt and shares outstanding of the company over the past few quarters.

I like the capital allocation of YUMC 0.00%↑ a lot, since the company is investing heavily in their own business to grow store count and make the supply chain more efficient (translates directly to the bottom line). Any cash that’s left over gets returned to shareholders via buybacks and dividends. CAPEX is expected to be in the range of 700-900 million USD for the year 2023. Meanwhile, shareholder distributions in the form of dividends and buybacks will be in the range of 600-800 million USD. Yum China might be one of the best capital allocators among Chinese large cap stocks, especially if we consider there recent buybacks.

5.0 Management

The quality and passion of the management is remarkable. I can recommend anyone interested in China or the business to listen the the latest conference calls by Yum China’s management team. Joey Wat is a fantastic CEO and she has navigated the company exceptionally trough tough times. Recently she said the following:

Winston Churchill once said, “Never let a good crisis go to waste.” Indeed, there are very few good things to say about the pandemic, but we made the most of it, and we strongly believe that every great company is the child of winter.

— Joey Wat; CEO of Yum China

Apart from Joey, the entire management team has done an exceptional job at making the best out of every situation. As a side note, Joey recently bought shares for 5 million HK$ at a price of HK $360 per share, 31% above the currently share price.

Lastly I want share the answer of the CFO on an answer in the last earnings call (the current market cap is 14.3 Billion USD):

6.0 Valuation

Yum China is arguably a great business. The question is, how much we are willing to pay for a business that will grow store count by 50% over the next 3 years, while improving efficiency and repurchasing shares at a fast pace. If we annualize the FCF generated year to date, we get to around 1.15 Billion USD. The exchange rates always fluctuate, but for simplicity I wont take this into consideration. The company makes FCF of around 81k $ per store (1.15 Billion /14.1k stores). If we expect 20k stores by 2026 and margins to improve slightly thanks to efficiency, then we get to around 1.7 Billion FCF by 2026 (at 85k $ per store). valuations for Dominos Pizza, McDonald’s, Yum Brands are all around 25x earnings. I know that it’s a Chinese company and that sentiment is extremely bad right now. But over the long run this will in my opinion normalize (at least to some extend). In a market in which quality is valued, YUMC 0.00%↑ could be worth around 20x FCF. But conservatively I will apply 15x FCF on 2026 numbers. This is already a market cap of ~26 Billion USD. If we also consider shareholder distributions of around 3 Billion that will have possibly even higher impacts (share buybacks at low prices), then a total return of around 100% is likely. Remember, Yum China isn’t a highly risky tech stock.

7.0 Conclusion

All in all, Yum China is a great company with impressive management skills. The Balance sheet is solid and the growth of the company is going to accelerate over the coming years. The Chinese middle class is a main driver behind the growth and will continue to be a tailwind for the company. The stock is undervalued compared to it’s quality and is returning excess cash to shareholders. If we look at the chart, we see that the stock of YUMC 0.00%↑ is at pretty significant lows, while the RSI indicator is suggesting that the stock is oversold on the weekly chart. 👇

I’m still in the process of deciding whether to enter a position yet, or wait longer and do more due diligence. If you have anything to add, don’t hesitate and write it down in the comments.

Yours sincerely,

MODERN INVESTING

Thanks for the write-up!

I did a write-up myself nuancing two of the main differences between Yum China Holdings and YUM! Brands.

https://jaminvest.substack.com/p/hk-4-yum-china-is-not-yum-brands

I agree with the overall thesis of your report, but things can change quickly. Restaurant Brands which owns KFC, Pizza Hut, Taco Bell in NZ, Aust, USA etc stock price is down 75% in 12 months with competition with Mickey Dees and others ramping up, cost pressures incl wage inflation, staff shortages, chicken costs soaring, insurance costs etc. Coupled with a surge in interest costs/rental increases as well profits which were large are now minimal at best. The outlook 18 months ago looked great similar to YUM, and it turned on its head in a manner of months. High fixed costs, margin compression and profits got wiped out overnight. Now a class action against KFC Australia for non payment of breaks, the CFO and CEO resigned/retired - dividends cut.