Colombian & Norwegian dividends keep flowing with oil making new highs

Colombian & Norwegian dividends keep flowing with oil making new highs

An update on Vår Energi, Geopark and thoughts on the FED’s monetary policy …

The general stock market is showing signs of a bubble. Valuations are getting insane, new investors are flooding the market and IPOs with negative earnings rally 50% in a day. It’s 2021 all over again! With the small difference, that there is a huge difference between tech stocks and the rest of the stock market. MAG7 is trading at large valuations and makes up around 29% of the market cap of the S&P 500. At the same time, small caps, commodities and foreign stocks (outside the U.S.) are trading near there lows.

In the following piece, I want to give updates and thoughts on Vår Energi and Geopark. Furthermore, we will look at how the FED’s actions/statements will benefit commodities.

1/ Vår Energi VAR 0.00%↑

Vår Energi has had some very interesting developments over last weeks, as the company hosted its capital markets day. The number o high profile investors holding the stock has gone up significantly, after Hitec Vision sold 220m shares via block trading.

Jan Haudemann-Andersen has been most exposed to technology and biotechnology on the stock exchange. Now he is buying into the oil company Vår Energi. The investor has bought one million shares for around NOK 34 million. Several high-profile investors have bought shares in Vår Energi recently. John Fredriksen, the Sundt family and salmon billionaire Helge Gåsø have increased their positions. The purchases come after the billion-dollar sale to major of HitecVision. Originally, the buyout fund wanted to sell 164 million shares, but it was not enough for the investors. The appetite was so great that the number of shares increased to 220 million.

Property baron Torstein Tvenge appears in another oil share. The investor has bought 100,000 shares in Aker BP for around NOK 27 million. The last time Tvenge was in Kjell Inge Røkke's oil company was in 2020.

— Finansavisen

Hitec Vision has been reducing the position in VAR 0.00%↑ since the IPO and has sold shares already in September of last year. The offering was several times oversubscribed back then and now is no different.

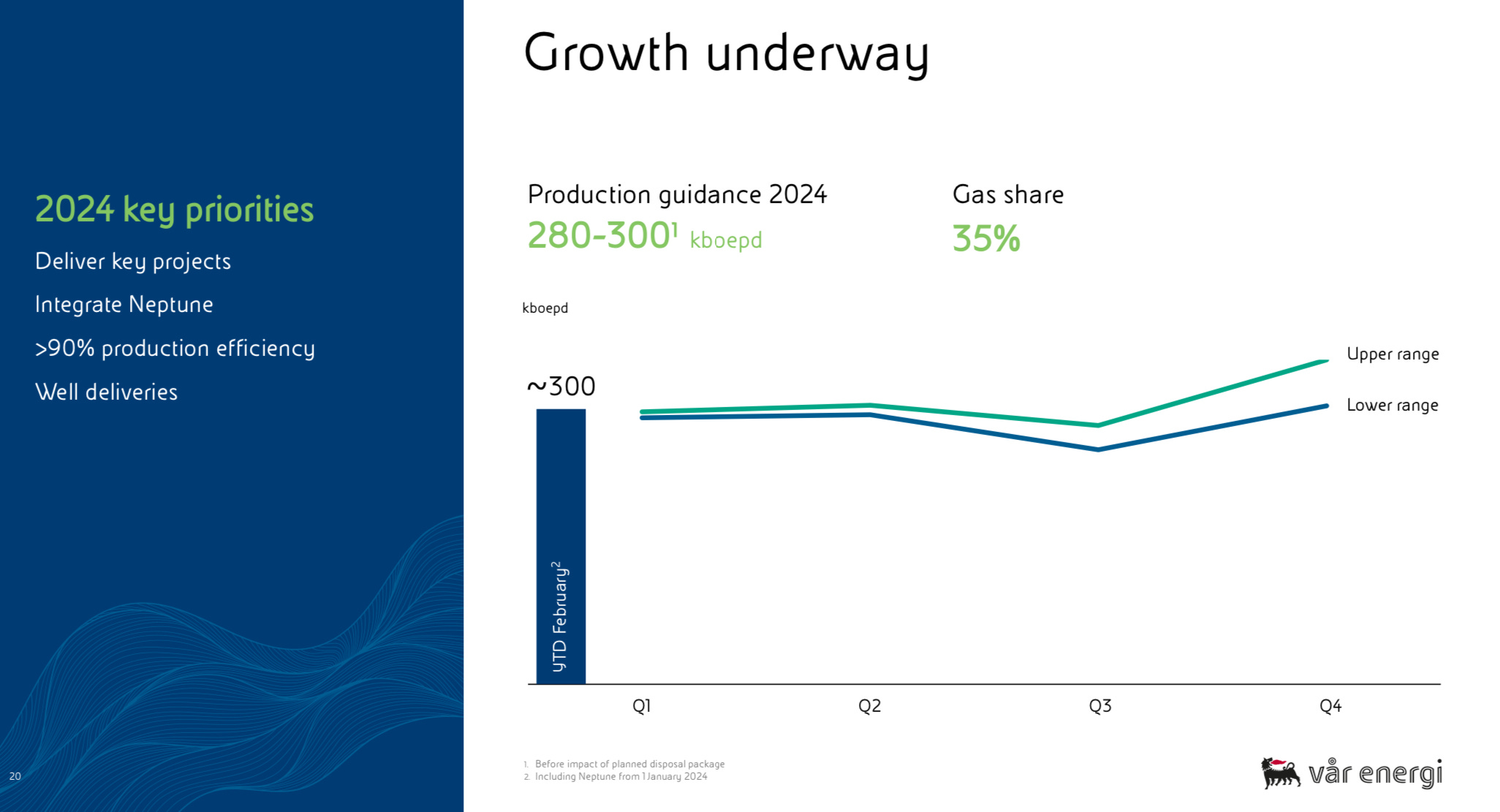

Apart from this event, the capital markets day has supported my underlying thesis in the stock. The key point of the presentation have been:

Production of 300k boe/d as of February, with a guidance of 280-300k boe/d for 2024. No changes to the plan of 400k boe/d by 2025.

1.24B boe in 2P reserves.

Synergies from the Neptune acquisition of around 500m $, instead of earlier expected 300m $.

22% ROACE (Return on average capital employed).

Balder X with a targeted production start as of Q4 2024 (no changes, but good confirmation).

OPEX per barrel should drop from 14$ to 10$ by 2025. Previously the company expected 8$. The increase in costs is primarily driven by inflation.

Reserve life index on 2P reserves of 12 years.

Reserves replacement ratio (2P reserves) of ~130% over the last 5 years.

Exploration costs per barrel <1$ .

Production to remain high till 2030, driven by more exploration and drilling.

With VAR 0.00%↑ we have to keep in mind, that the company is currently at its CAPEX peak. Once CAPEX starts to fall (2025) and production is higher, FCF will increase massively. Also new production coming online will have lower operating costs, resulting in tailwinds for the company. While we wait for production to ramp up, we are getting paid a 15% dividend yield.

There are also risks. The 2 main risks are firstly, that there could be delays regarding new production coming online. Secondly, debt is quite high. The company has interest bearing debt of ~3.8B $ and current assets of 1.3B $. This equates to Net interest bearing debt of 2.5B $, while they invest most of their cash flows into new production and dividends. This is obviously not sustainable, but once FCF starts moving higher (2025), the company should be able to avoid problems.

The first debt maturity is in 2026, which means that the company has time to ramp up production, increase FCF and its cash balance. In addition, the company generated FCF of 779m $ in 2023, which is nearly enough to pay for dividends.

Investors are buying a lot of shares of VAR 0.00%↑, which makes me confident, that even in a case of difficulties, the company could/will refinance some of it’s debt. Vår has been able to refinance a bond till 2083 (!), which shows us that they will be able to manage the situation.

2/ Geopark GPRK 0.00%↑

Geopark has performed well over the last weeks, following the pitch of mine (17th of February). This was mostly driven by Geopark reporting annual results for 2023 and the announcement of a tender offer worth 50m $ (10% of the market cap at the time).

Buying back 10% of the shares outstanding at a price between 9 and 10$ a share is highly supportive for the share price. This is a measure that all highly undervalued small caps should implement, to reward shareholders. In addition to the 10% tender offer, there is a regular buyback programs, which will be finished by December 2024. This buyback is for an additional up to 10% of the shares outstanding!

The company is performing well, the management is doing all the right things to benefit shareholders and the oil price is moving higher. I remain highly bullish on the stock and think that the risks regarding Colombia are overblown. Petro (president) has not much power, with the senate being against him.

The new attorney general isn’t a supporter of Petro, which demonstrates that his power and influence is declining. Recently the Colombian senate shelved Petro’s Health Reform Bill.

It’s pretty clear, that politics is what has resulted in the low valuations of Colombian stocks. While his power is shading, he is playing games and gets attention here and there. The bottom line is that his term will end in 2026 and that he hasn’t much power anymore. In the mean time, valuations for Colombian stocks are among the lowest in the world.

Something, that I think will change once the rate cuts of the Colombian Central Bank have an effect. South America has among the best central bankers in the world and is currently cutting rates from the huge levels they are at right now.

3/ Conclusion

In January I wrote a post called: “Back to the Future: The Economic Deja Vu of the 2020s mirroring the 60s and 70s”. 👇

Back to the Future: The Economic Deja Vu of the 2020s mirroring the 60s and 70s

I compared the 60s/70s with today and concluded, that inflation is likely to follow a similar pattern as 50 years ago. On Wednesday the FED signaled 3 rate cuts for 2024, while holding rates steady.

Jerome Powell emphasized that the U.S. economy is strong and growing at a fast rate, while unemployment is low. My simple question is, why would the FED have to cut rates when the economy is so strong? Rates should just stay at the levels they are currently at, and do there job. But political pressure on the FED is rising (election year). And if we look at commodities, then they are telling us that rates will be cut. They are screaming inflation with Gold at an ATH and oil moving higher.

In short, I see the statements by the FED as bullish on commodities, but try to stay away from U.S. stocks. Espeacilly tech is overbought and is in for a big correction. The question is not whether there will be a crash in the high flying, overvalued, mania stocks, but when the crash will occur. Cheap oil & gas stocks that return cash to shareholders are a good hedge against inflation and geopolitical instability.

Yours sincerely,

MODERN INVESTING

Have you ever looked at Petrotal? Could be interesting addition to GPRK/PRX for jurisdiction diversification

Thanks for the the article.

There is not much information around for geopark , so i appreciate that you picked this up.

Apparently Calvin has stopped talking about his oil-picks.